Dwola Payments Infrastructure: ACH Automation, API Integration & Business Controls

Introduction

Bank-to-bank transfer systems remain a critical component of digital finance in the United States. Many SaaS platforms, marketplaces, and fintech services rely on ACH rails to move funds efficiently between verified accounts. API-driven payment infrastructure enables these businesses to automate transactions directly within their applications.

Dwola is frequently referenced in conversations about ACH-based payment APIs. This article provides a structured, neutral explanation of dwola, its technical architecture, operational capabilities, and regulatory considerations. The information is intended for educational purposes only.

What Is Dwola?

Dwolla is a financial technology provider that offers ACH payment infrastructure through an API-first model. Instead of serving as a consumer-facing wallet, dwola enables businesses to embed direct bank transfer functionality into their own platforms.

The platform’s primary focus is facilitating account-to-account transfers via automated clearing house (ACH) networks.

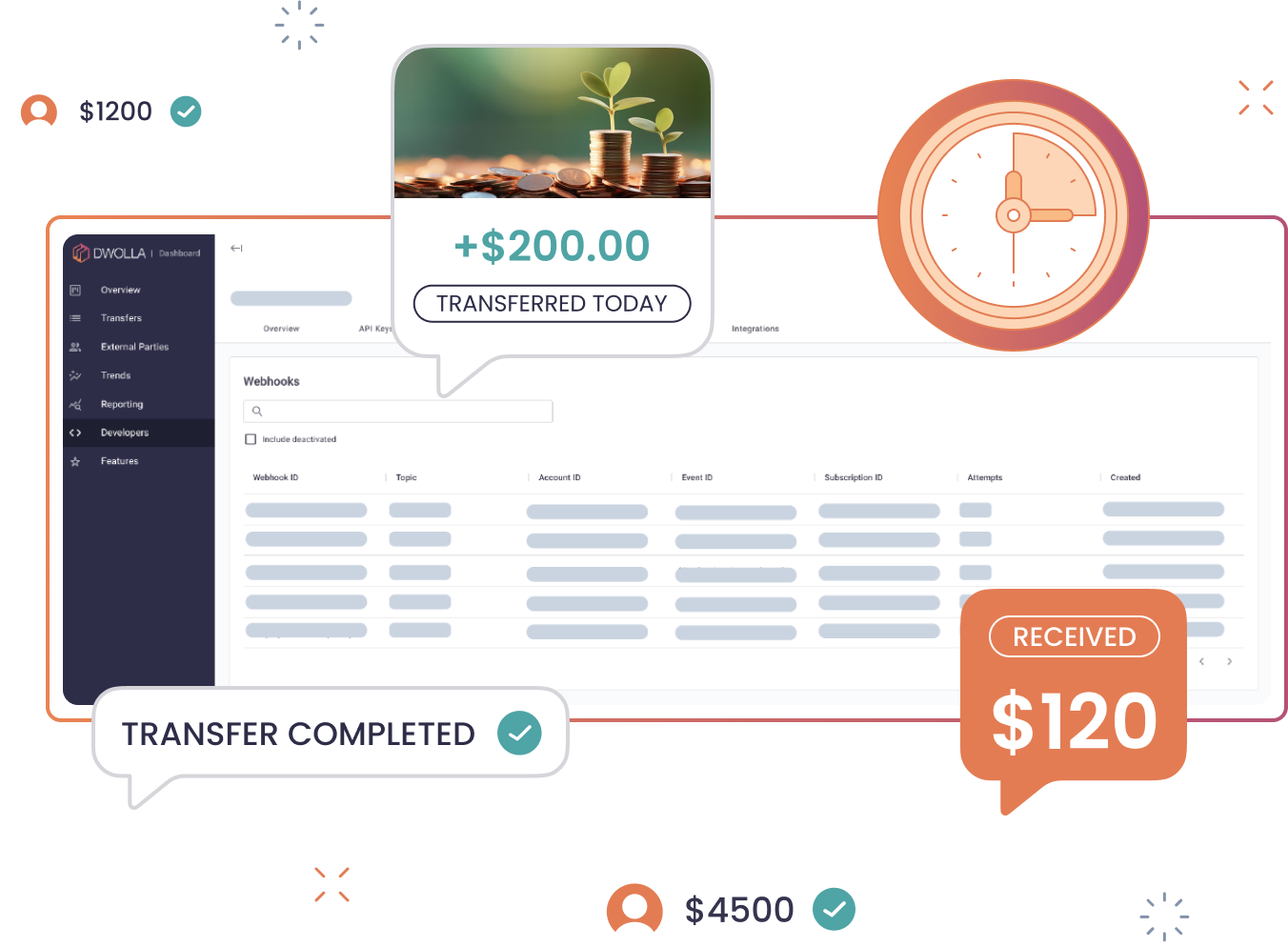

Technical Architecture & API Model

4

Dwola’s infrastructure is typically built around:

- REST-based API endpoints

- Secure token authentication

- Webhook notifications for transaction updates

- Sandbox testing environments for development

This architecture allows developers to initiate transfers, track payment status, and manage account verification programmatically.

Core Capabilities

Dwola may support the following functions:

ACH Transfers

Direct movement of funds between verified U.S. bank accounts.

Recurring Payments

Scheduled billing workflows for subscription-based services.

Mass Payouts

Distribution of funds to multiple recipients, commonly used in marketplace models.

Bank Account Verification

Processes to confirm account ownership before initiating transfers.

Business Applications

Dwola infrastructure may be implemented in:

- SaaS subscription platforms

- Marketplace payout systems

- Fintech applications

- B2B invoicing automation tools

- Platform-based service providers

Implementation details vary based on transaction volume, compliance requirements, and integration complexity.

Compliance & Regulatory Framework

ACH-based payment systems operate under regulatory oversight. Organizations evaluating dwola should assess:

- KYC (Know Your Customer) requirements

- AML (Anti-Money Laundering) procedures

- NACHA operating rules compliance

- Data encryption standards

- Partner financial institution arrangements

Compliance review is essential before launching live payment flows.

Security & Risk Management

Dwola generally incorporates security controls such as:

- Encrypted API communications

- Role-based access permissions

- Authentication token management

- Monitoring systems for unusual activity

Security frameworks should align with internal governance and risk policies.

Integration Workflow Overview

A typical dwola integration process may involve:

- Registering for developer access

- Generating API credentials

- Testing transfers in sandbox mode

- Configuring webhook listeners

- Completing compliance onboarding

- Deploying to production

Comprehensive testing helps reduce operational risk.

Dwola Compared to Card-Based Payment Systems

| Feature | Card Processors | Dwola |

|---|---|---|

| Card Network Dependency | Yes | No |

| ACH Specialization | Limited | Core capability |

| API-First Design | Varies | Yes |

| Recurring Bank Transfers | Supported | Supported |

| Direct Account-to-Account Transfers | Partial | Primary function |

Dwola’s focus on ACH rails differentiates it from card-centric processors.

Operational Considerations

Before integrating dwola, businesses should evaluate:

- Expected transaction volume

- Settlement timing requirements

- Return and reversal procedures

- Fraud mitigation controls

- Technical resource availability

Structured planning enhances payment stability.

Conclusion

Dwola provides ACH-based payment infrastructure through a developer-oriented API framework. Businesses seeking embedded bank transfer functionality may evaluate dwola as part of broader payment strategy planning. Regulatory compliance, technical readiness, and operational testing are critical before deployment.

This content is informational and does not constitute financial or legal advice.